For the past 1 year, the only profitable “investments” in my portfolio are essentially USD and Singapore Saving Bonds. Even though they have yielded at best 3% to 5%, the relative outperformance is huge since most other stuff are easily down by 30%.

Some discipline in portfolio allocation (70/30) has probably saved my ass from DCA-ing too heavily into the downward spiral of HK equites and crypto. And honestly, for that 30% non-volatile “bond” component, I believe there is nothing with a better reward/risk ration than Singapore Saving Bonds (SSBs).

So if I am subscribing for this month’s SSBs, it’s pretty obvious I have subscribed for the previous few months’ offerings (higher rates) as well.

And now, even though some Fixed Deposits, T-Bills or Singapore Government Securities (SGS) bonds are offering higher yields than the headline 2.75% rate, I am still going with SSBs. Financial Horse wrote a comprehensive article on this which I largely agree with. Let me flesh out some of the key points:

1. Liquidity

The SSB is very very liquid. For example, if you were to apply to redeem any of the previous batches of SSBs today on the 21st of September, the funds will be in your bank account on the 3rd of October, 12 days later.

Personally, I do believe it’s ok to even park the a significant proportion of your emergency funds in SSBs since there are very few emergencies that cannot wait for a month, not to mention 12 days.

Depending on the calendar month and the business days, the redemption period could range from as short as 4 days to as long as 36 days. If you were to take the average, that’s about 20 days or three weeks, which I find perfectly reasonable.

Apparently (I have no personal experience interacting with it), T-Bills are very difficult or close to impossible to sell if you suddenly need the liquidity.

So I do believe the slightly lower yield is a small price to pay to retain liquidity in case the market experiences a sharp crash and I need to liquidate my bonds to restore my “asset allocation” to the desired ratio and implement some form of “buy low, sell high”.

2. Capital Guarantee and Pro-rated Interest On Redemption

“You can redeem your Savings Bonds in any given month before the bond matures, with no penalty for exiting your investment early. “

This is what the SSB promises. If next month’s rate increases, you can simply redeem the previous month’s issue at par value and apply for the next issue. This is probably the closest to a free lunch. At the same time, you will receive any accrued interest upon redemption

Whereas for Fixed Deposits, an early redemption means that there are penalties and you will likely have to forego some if not all of the accrued interest.

3. Simplicity

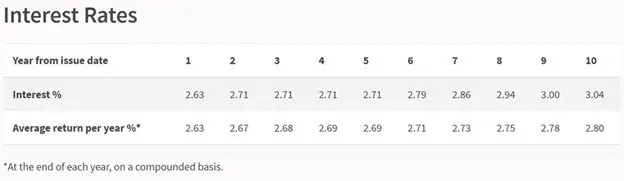

The above table for the latest T-Bill is not that easy/simple to interpret for a layman. Especially if compared to this.

But basically, the yields for T-Bills and SGS are only determined after the auction is over, not at the point when you ballot for it. That said, it generally will not be too different from the previous issue, but you are sort of locked in till maturity unlike the SSB.

Downsides of SSB

Needs to be 18 year old and above so sadly, my baby cannot qualify. But I guess the main gripe is that it’s hard to get a good allocation when the yields are good. For some of the recent issues, it was hard to even get a small 5 digit allocation.

And there is also a $200k cap for each individual. But actually, from a household point of view, if you include your spouse or your parents (or people you trust), the cap would expand and most people would have plenty of buffer.

If you have plenty of liquidity idling around, then of course, that’s where the Singapore Government Securities (SGS) bonds and T-Bills come in.

That said, it’s likely that I will participate in the next few SGS or T-Bills auctions to understand the process/mechanism a bit better. Not that I need it but I guess it might make sense to “guide” my in-laws to do it for their SRS accounts and CPF OA accounts.

Thanks for reading!

One Reply to “Subscribing For This Month’s Singapore Savings Bond (SSB)”