In case you are wondering, I have not been selling “risky” assets like stocks, REITs and crypto in the past few months to put more into relatively safe investments like Singapore Saving Bonds (SSBs).

Yes, in a rising interest rate environment where fixed deposits and T-bills are yielding around 4%, coupled with declining stock prices, it is tempting to sell everything and park it in high-interest cash instruments. Theoretically, one could always buy back the risky assets at a lower price.

However, since I have proven to be not that great a market timer, I prefer to stick rather closely to my asset allocation, which is 70:30 in “risky” assets’ favour. Honestly, I am tempted to go to 80:20 since we are in a bear market but the “this time it is different” vibe is holding me back.

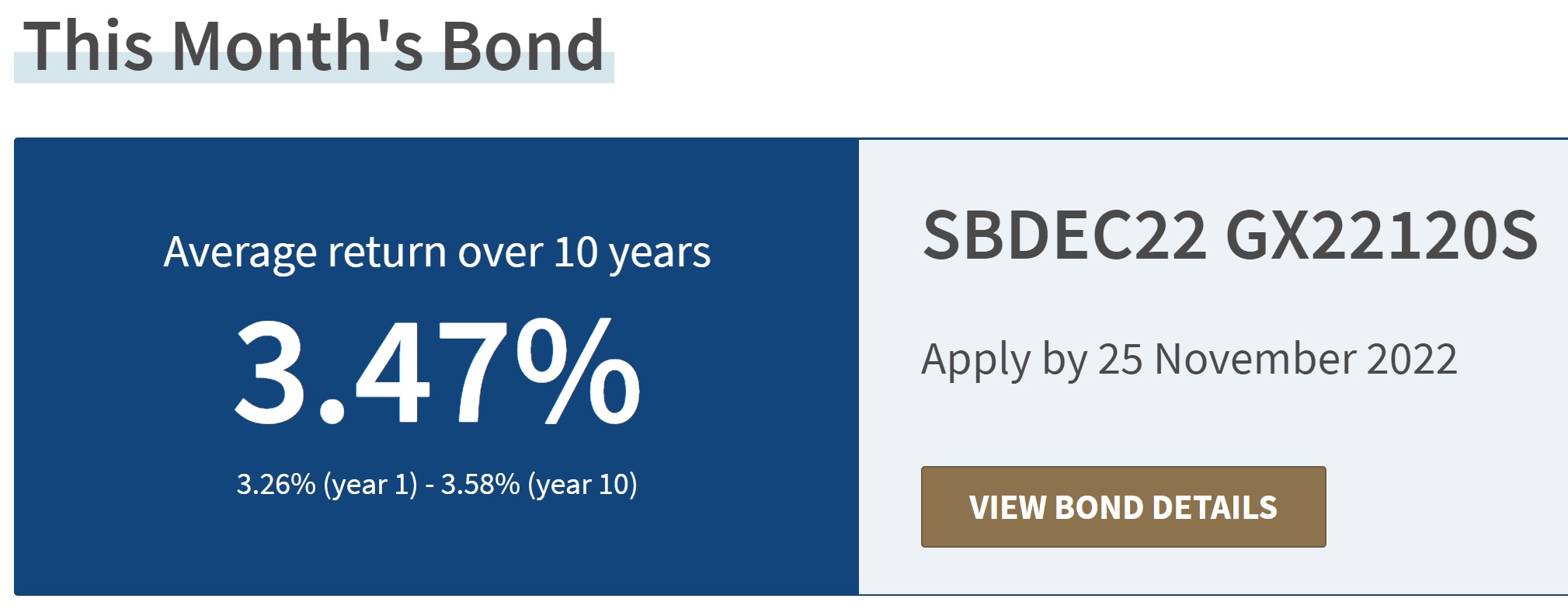

Dec 2022 SSB

So in a sense, I do have very limited cash to take advantage of this latest high-yield SSB, with its details below.

This is the best SSB to date so personally, I do believe it is imperative to apply for it. 3.47% is also probably higher than the effective rate of a CPF voluntary contribution.

If you are interested and have not applied for it, do note that the closing date is today on 25 November.

I am expecting allocation to be capped in the region of ~$10,000.

Which SSBs Am I Redeeming?

Since low-yielding cash reserves have been quickly depleted (a good thing), it is also finally time to utilise SSB’s secret feature, the ability to roll-over SSBs without any penalty*.

*Do note that applying and redeeming costs $2 each, so please do not constantly apply and then redeem $500 of SSBs since the additional returns of will not offset the costs.

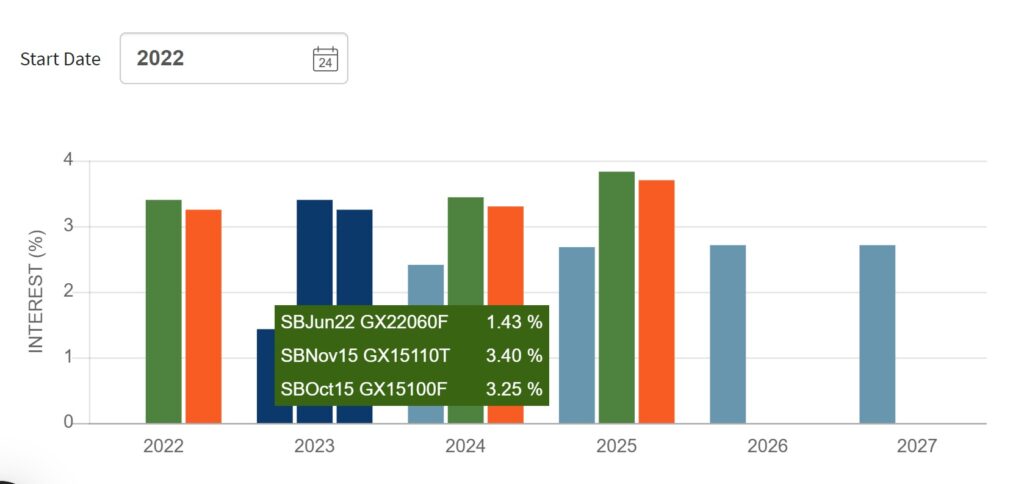

In case you are unaware, MAS has designed a great website for us to check on our SSB portfolio using our Singpass. So there is no need to manually compile and update every time you apply or redeem for an SSB.

There is also this great feature where we can select up to three of the bonds for comparison.

In the above diagram, I have compared the issues of Jun 2022, Nov 2015 and Oct 2015. The two 2015 issues are approaching maturity in 2025 and are expected to yield >3.5% for the next three years. So unless short-term yields further rise above 4.5%, I am unlikely to redeem the Nov 2015 and Oct 2015 issues.

On the other hand, Jun 2022 seems to pale a lot by comparison and appears to be the likely candidate to be redeemed.

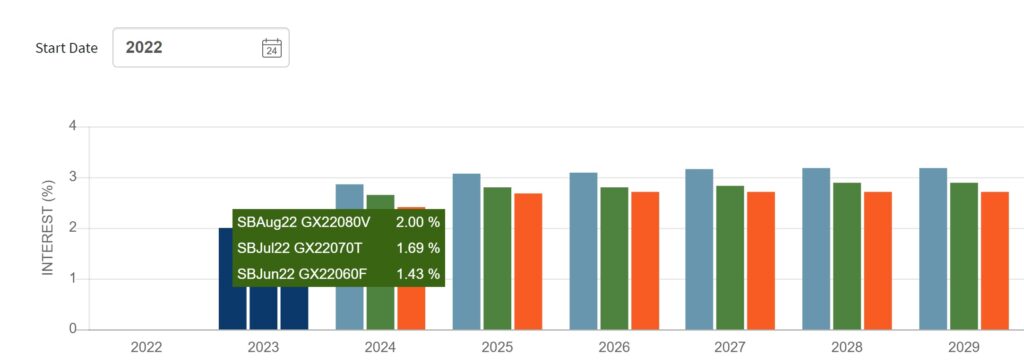

I realised I needed to be fair to Jun 2022 and compare it peers who are around the same age as him, notably Jul 2022 and Aug 2022.

The difference is not so stark this time but it is also clear that Jun 2022 will provide a lower return compared to the other issues. Not surprisingly, since rates were rising rapidly in the second half of 2022.

Therefore, just by making two sets of comparisons, I have decided to fully redeem my Jun 2022 SSBs.

Conclusion

If your cash is starting to run low like me, do consider redeeming past issues of SSBs that are now unattractive in this current interest rate environment. To do a quick comparison in less than 5 mins, do log on to the SSB portal.

And then, finally, redeem the SSB with the lowest future return!

Thanks for reading.

If you enjoyed this article or found it useful, do subscribe to my blog via email to receive notifications of new posts.

Do follow me on social media for updates too!

Thanks for the support!

Personally, I am irritated by ads and pop-ups so I do not use any of them on this blog too.